Why America's Empty Offices Are About to Become a Banking Problem

Roughly $900 billion in commercial real estate loans mature in 2026, into a world where money is twice as expensive and buildings are worth a third less. The losses land squarely on the regional banks that became America's biggest property lenders.

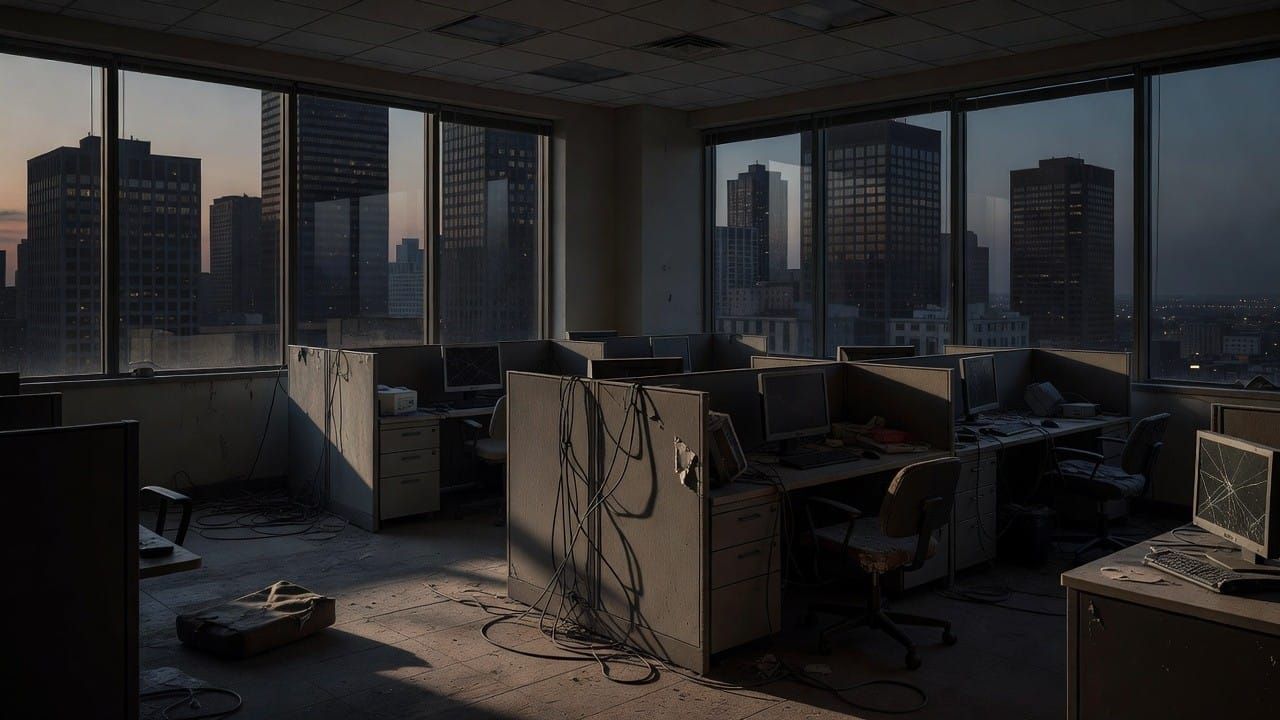

Somewhere in midtown Manhattan stands a 50-story tower that was worth $400 million in 2019. The elevators still run. The lobby is still polished. But four floors are leased, the loan that financed it comes due this year, and no lender on earth will refinance it at anything close to the old price. The building's owner has two options: wire tens of millions in fresh equity to keep it, or hand the keys to the bank.

Multiply that building by thousands, and you have the story of 2026.

This is the year America's commercial real estate reckoning stops being a slow-motion abstraction and becomes a hard number on bank balance sheets. Roughly $900 billion in commercial real estate loans mature in 2026 — and more than $1.5 trillion comes due before the year is out. Most of it was borrowed when money was nearly free. All of it has to be refinanced into a world where money is expensive and the collateral is worth a fraction of what it used to be.

The question isn't whether this hurts. It's who absorbs the blow — and the answer points squarely at the regional banks that quietly became America's biggest landlords-of-last-resort.

The Wall Everyone Saw Coming

The mechanics are almost insultingly simple. A wave of commercial mortgages was written between 2019 and 2022, when interest rates sat at 3 to 4 percent. Commercial loans don't amortize like a home mortgage — they typically run five to ten years and then come due all at once, with the assumption that the borrower will simply refinance into a new loan.

That assumption just broke.

Those loans are now maturing into an environment where comparable financing costs 6 to 8 percent. Meanwhile the buildings backing them have lost value — office properties in particular are worth, in many cases, 16 to 35 percent less than they were at origination. So a borrower facing maturity confronts a brutal arithmetic: the property is worth less, the new loan costs roughly double, and the lender wants more equity in the deal, not less.

For a trophy tower in a thriving market, the owner writes a check and moves on. For a half-empty office building in a city center that never recovered from remote work, there is no check large enough to make the math work. The loan goes into "special servicing," then into default, and eventually the property changes hands at a price that crystallizes the loss for whoever held the debt.

That is the maturity wall. It is not a forecast. The loans exist, the maturity dates are on the contracts, and the calendar is non-negotiable.

Why Offices Are the Epicenter

Not all commercial real estate is in trouble. Data centers are on fire — in the good way, fueled by the AI buildout. Industrial and logistics property remains tight. Even apartments, despite oversupply in some Sun Belt markets, generate rent every month.

Offices are different, and the data is unambiguous. National office vacancy sits near record highs, with major markets running above 20 percent — meaning one in five square feet sits dark. The sector has now logged four consecutive years of cumulative occupancy losses. Hybrid work didn't kill the office, but it permanently shrank how much of it companies are willing to pay for.

The distress numbers have turned from worrying to alarming. The office loan delinquency rate jumped 156 basis points to 13.9 percent in January 2026 — driven in part by landmark defaults like One New York Plaza, an $835 million loan that tipped into special servicing ahead of its maturity. Across rated commercial mortgage-backed securities, the 30-plus-day delinquency rate climbed to 8.1 percent, and offices accounted for nearly 70 percent of all newly distressed loans.

When a third of a sector's debt is delinquent or distressed, that is no longer a cyclical wobble. It is a structural repricing of an entire asset class — and somebody is sitting on the loans.

The Quiet Problem at the Regional Banks

Here is the part that should hold an investor's attention. The losses from this maturity wall are not evenly distributed across the financial system. They are concentrated, by design, in the institutions least equipped to absorb them.

Roughly 70 percent of all outstanding commercial real estate loans sit on the books of smaller and regional banks, not the money-center giants. For a large diversified bank like JPMorgan, CRE is about 13 percent of the balance sheet — a manageable slice. For the typical regional bank, it is closer to 44 percent. More than half of regional banks now exceed the 300 percent CRE-to-capital ratio that regulators flag as a concentration red line. Regional institutions alone hold an estimated $396 billion of the debt maturing this year.

The reason is historical. When big banks pulled back from commercial real estate lending after the 2008 crisis, regional and community banks rushed in to fill the gap. It was profitable, relationship-driven business — and for a decade, with rates low and buildings full, it worked beautifully. The same concentration that powered a decade of regional-bank earnings is now the concentration that threatens them.

The cautionary tale already has a name: New York Community Bancorp. NYCB, with roughly 60 percent of its loan book in commercial real estate, has posted multiple consecutive quarterly losses and was found to be dramatically under-reserved on its office exposure — holding reserves near 2 percent against office loans where larger peers were carrying 8 percent or more. The market's fear is not that NYCB is uniquely reckless. It's that NYCB is simply the first to report honestly, and that dozens of similarly concentrated banks are carrying loans on their books at values the open market would never validate.

What It Means for Your Money

This is where the story stops being about real estate and starts being about the financial system — and your portfolio.

This is not 2008, and it's important to say so plainly. The CRE maturity wall is large, but it is a known, dated, and largely ring-fenced problem. It will not detonate the entire banking system the way subprime mortgages — buried inside opaque derivatives across every major institution — once did. The losses here are visible and traceable. That is genuinely reassuring.

But "not systemic" is not the same as "not painful." Three things are worth watching.

First, regional banks are the pressure point, not the megabanks. The KBW Regional Banking Index is the cleaner read on this stress than the broad financials sector. Concentration matters more than size; a $20 billion bank with 45 percent of its book in office loans is more exposed than a $2 trillion bank with 13 percent across diversified property types. The banks that quietly disclose elevated CRE reserves over the next several quarters will tell you where the bodies are.

Second, a credit crunch can spread even when defaults don't. Banks bracing for CRE losses pull back on all lending — to small businesses, to homebuyers, to other developers. That tightening is a real drag on the broader economy, and it happens regardless of whether any single bank fails. The macro risk here is slow strangulation of credit, not a sudden crash.

Third, distress creates buyers. Every dollar of forced selling is a dollar of opportunity for someone with capital and patience. Private equity real estate funds, opportunistic credit shops, and well-capitalized REITs have raised enormous "dry powder" specifically to buy distressed buildings and loans at the bottom. The maturity wall that wrecks an overleveraged regional bank is the same wall that hands a generational entry point to a disciplined buyer of quality property at 60 cents on the dollar.

The Bottom Line

The empty office tower is the most visible symbol of a problem that is fundamentally financial. The buildings didn't change overnight — the cost of money did, and a decade of cheap-rate lending is now being marked to a market that no longer exists.

2026 is the year the bill arrives. It won't bankrupt the country, and it won't repeat 2008. But it will quietly reshape the regional banking sector, tighten credit across the economy, and transfer enormous amounts of property from those who borrowed at the top to those who held cash for the bottom. The maturity wall doesn't care about narratives or hope. The dates are on the loans, and the calendar always wins.

Get this level of intelligence every day. Subscribe to AlphaBriefing — free, member, and paid tiers available.

Sources & Further Reading

- S&P Global — Commercial real estate maturity wall: $950B in 2024, peaks in 2027

- Congressional Research Service — Commercial Real Estate and the Banking Sector

- Cohen & Steers — Putting recent commercial real estate debt headlines into perspective

- Bisnow — CRE Lending Exposure Could Mean Fresh Trouble For Regional Banks

- CRE Daily — Maturing Debt Drives 2026 CRE Distress

- Wharton — Too-Many-to-Ignore: Regional Banks and CRE Risks

Disclaimer

AlphaBriefing is an independent intelligence publication. The content in this article is produced for informational and educational purposes only. Nothing published by AlphaBriefing constitutes financial, investment, legal, tax, or regulatory advice, nor should it be construed as a solicitation or recommendation to buy, sell, or hold any security, asset, or financial instrument.

All views expressed are those of the author at the time of writing and are subject to change without notice. Markets are volatile and unpredictable; past performance is not indicative of future results. Any investment involves risk, including the possible loss of principal.

AlphaBriefing and its principals, employees, or contributors may hold positions in securities or assets mentioned in this article. This should be considered a potential conflict of interest. No material relationship with any company referenced exists unless explicitly disclosed. Readers should conduct their own due diligence and consult qualified financial, legal, and tax advisors before making any investment decisions.

Information in this article is drawn from public sources believed to be reliable at the time of publication. AlphaBriefing makes no warranty, express or implied, as to the accuracy, completeness, or timeliness of any information herein. AlphaBriefing accepts no liability for any loss or damage arising from reliance on this content.

© AlphaBriefing. All rights reserved. Unauthorised reproduction or distribution is prohibited.